The mortgage brokers provide their services free of cost to the customer. They deal with different lenders and can provide the options most suited to your circumstances. They access your needs and identify your loan requirements accordingly. Using a mortgage broker gives you more options – they look at multiple lenders, not just banks, to find the loan which is right for you.

We will complete all the mortgage applications for you to ensure your home loan application has the optimum chance of success. Our custom mortgage broking software compares all mortgage rates so we can deliver you the best value home loan for your situation.

In most cases, it is seen that people like to fix the interest rate on their loan for certain period like 1 to 2 years or more, so it gives more certainty to their household budget, but in some situations, it may be more advisable to have the loan on floating interest rates or a combination of both. It all depends on your situation, the analysis of which we can help with. In New Zealand, currently the banks are offering the historical lowest ever interest rates, ever seen in this country.

Most of the banks require documents to prove your income and your deposit that you propose to contribute, together with your bank statements to verify your personal expenses pattern and your account conduct. The banks also require knowing of your current assets and liabilities. They usually require your residency status proof to process the application.

Most of the banks require 5 to 10 working days to access the application. In some cases, it may vary depending on the urgency of the application.

Normally, the banks require minimum of 20% deposit. A minimum of 30% to 40% deposit for an investment property. Normally a deposit of 35% will be required as a minimum for commercial properties but it can vary depending on the particular situation.

You can be eligible for the home start grant as per below:

a- $1,000 for each completed year of kiwi saver membership, subject to a maximum of $5,000, if you are purchasing an old existing home.

b- $2,000 for each completed year of kiwi saver membership, subject to a maximum of $10,000, if you are purchasing a brand-new home.

c- And provided you meet the following conditions:

(i) – You have been contributing to kiwi saver for a minimum of three years

(ii) – You are purchasing the house for living in there and not for renting out

(iii) – Individual income no more than $85k p.a. and household income no more than $130k

(iv) – The maximum purchase price should not exceed $600k for old house and $650k for brand new house if purchasing in Auckland. There are limits for other parts of the country – talk to us for more information.

How much money can I save by refinancing?

Depending on each individual situation, the customers can save thousands of dollars by restructuring or refinancing their mortgage.

Total Assurance can offer you the best, honest and free advice in all types of risk insurance and general for both individuals and businesses/corporations, no matter what the size. This includes:

Life Insurance

Medical/Health Insurance and Group Medical Insurance for Businesses.

Trauma Insurance

Income Protection and Redundancy Cover

Mortgage Protection Insurance

Key Person Insurance Cover

Total Permanent Disablement Insurance

Household expense cover

With our relationship with New Zealand’s top insurance providers, we can often negotiate better deals for your cover than you will find alone. A lot of times many people can end up paying more than they need to for their insurance by not having the right sum assured or not having the right type of cover for them entirely. Total Assurance will personally take the time to know your exact circumstances and put an accurate cover in place for you.

The answer to this question will vary depending on your own personal needs from your insurance plan. There are several factors which need to be considered when choosing a provider. Every company is slightly different in the way that it structures its cover. Insurers have different way of processing claims for medical/surgical treatments (health insurance) or in the event of the policy holder’s death (life insurance). Therefore, the service we provide can be so beneficial to you, as our knowledge of each company is unmatched, and taking your personal situation into account, we can quickly and easily find the best insurance option specifically for you.

Making claims can be extremely stressful and add a burden to you during already hard times. That is why our insurance service to you offers free claims management to take the stress out of your hands and make sure you get the claims you need quickly, easily, and efficiently. We have an unmatched history of getting results at claim time and this is part of the service we offer to all our clients completely free.

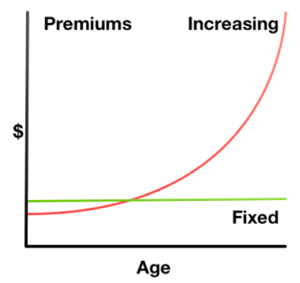

In general, yes. Your age is one of the primary factors influencing your life insurance premium rate, whether you are seeking a level (fixed premium) or stepped (annually increasing premium) option.

Stepped Premium Option: Premium will increase on your policy’s yearly anniversary based on age, inflation and below few factors:

New medical technology (more costly to provide treatment).

Rising medical inflation (increasing consultation, treatment, and equipment costs).

Level Premium: Your premium will not increase based annually. you can get terms of 10, 15, 20, 30 years or till age 65, 70, 80 etc. The premium is guaranteed not to increase for the life of the term period. The longer the term period, the higher the premium because the older, more expensive to insure years are averaged into the premium

People who smoke will have to pay a higher insurance premium. Many people are surprised that insurers often consider a person who smokes even just a few times a week or month to be a smoker. If you successfully

quit smoking for at least 12 months you can apply to have your premium reduced; and we can help you with this.